I had thoughts about how to title this article. I originally wanted it to be "The Doom of Civilization", but I realised it was too dramatic, even for me. After a few iterations I settled on the tille you're seeing now.

1. Push to digital

In today's world, almost everything is digital. Except for brushing teeth and bathing. For now. Your banking, access to money is online. Cash is seemed as sin. If you withdraw cash, you must be up to no good (in fact you get questioned if you withdraw a substantial amount of money). Payments are now online. From buying groceries, food and almost everything is powered by online payments (QR based or app based). Communications are online, telegrams don't exist anymore, very rare you get a handwritten letter or even a greeting card (I remember having a stack of at least 20 physical deepavalli greeting cards to be distributed every Deepavalli, and my mother makes it a point to hang the cards we received on the wall). Those days are gone. I still remember the elders would start crying the minute the postman announced that there is a telegram to the home (telegrams often carry bad news, notifications of dearly departed). Good news, no more wailing. It's replaced with a nice graphics sent over WhatsApp.

2. Ecosystem of digital

The completeness of the ecosystem depends on all the process either leading or already is digital. For example, you have the "Know Your Custimer" process before a bank account is created. That involves verifying your identity documents, be it manual or electronic (depending on which part of the world you are), and you're onboarded (meaning your account is created). Hence you have just joined the large fraternity of online banking, with access to everything banking, online. Same goes to other processes. This creates a mesh of internetworked, interdependent systems and even data. For exmaple, a person's national ID is supposed to be lifetime. No changes (legally) is made to that identifier. That, and also your mobile number and email address becomes a key identifier and identity to your online presence. Coupled with password or any other supposed authentication mechanism which "protects" your credentials, and gives access to the functionalities and your data.

3. Problems in wonderland

I studied IT more than 20 years ago, and I was a strong proponent to digital. I beleived that digital would revolutionise the world and make the world a better place. Looking at where I stand right now, a lot of what I believed had come true. From the days of 9600 baud dialup internet accessing gopher sites, looking at the advent of World Wide Web and the Internet as we see it today, humanity has moved leaps and bounds when it comes to IT.

But it didn't come with just wins.

The death of digital is digital itself.

Your life, whether you chose to see it, now is dictated by technology.

If your bank says you have RM10 only in your account, you only have RM10. Account passbooks? They dont exist anymore. You probably would have heard of the 1 Cent Thief, made into a TV drama. In today's world, it would be literally impossible to track such fraud. There is no independent data storage or management by the user vs. the organization. You simply have to "trust" that the system is right, always.

Systems can and will fail due to many reasons. Cybersecurity is one such risks which is highly flagged, requires a lot of investment, often under-invested and lacks the right level of maturity judging from the organization it's in.

The Malaysian government promotes Cybersecurity in every nook and corner, slating the introduction of Cyber Security Act as a cornerstone for cybersecurity. Heck we even have a Ministry dedicated for it, a specialist government agency on cybersecurity (CSM) and a national level coordination committee (NACSA). Yet recently (june 2026) a number of government websites were defaced, by Anonymous and other groups. The same isn't far for other organizations, be it public or private sector.

I've also written how organizations have poor standing in managing technology. In one case, obsolescense was poorly managed with the mantra "If it ain't broken don't fix it", which resulted in a massive failure. Lack of technology aware senior leadership and board members compound this issue, while the blame is often pushed to the working level (someone was fired, took the company to court and won, in Malaysia).

In the advent of a catastrophic failure of your IT/technology system, can your business operate normally without any disruption?

You'd ask me the same thing - since I have a website. I have a backup copy which I can restore anytime. But it does give rise to a thought. Maybe I should write a book, compiling all these articles? Then its completely foolproof. (that has to be physical, what you can touch kinda paper book)

4. Actual situation that spurred this article

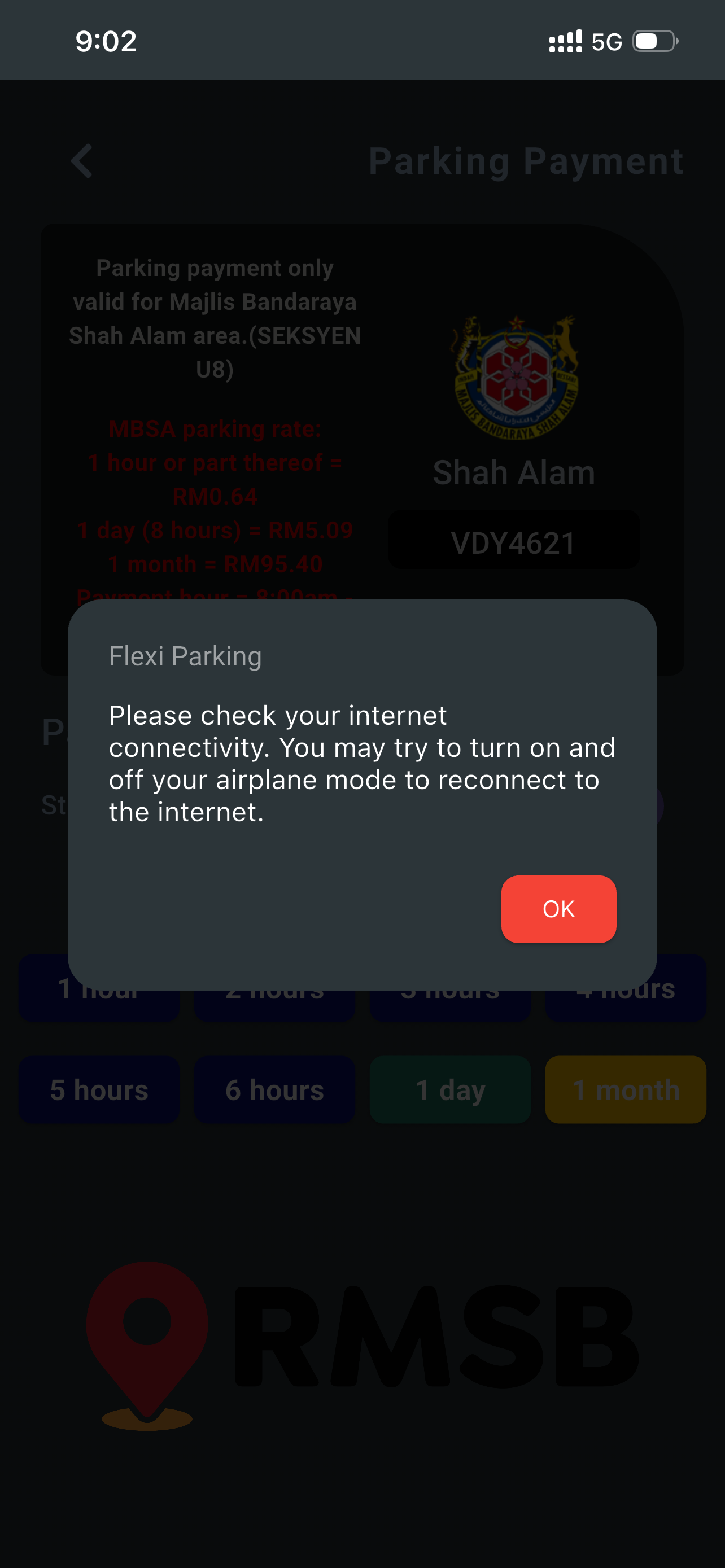

So this is what happened which caused me to think about this topic. This morning, just like any other morning, I head out to my favorite mamak to have my nasi lemak and teh 'C'. Since I am parking at the usual car park lot in front of the shop, I'd to pay parking. I fired up Flexiparking and attempted to make payment. Failed. Tried a few times, also failed.

So I thought maybe Flexiparking is having a bad day. I tried TnG next. Also failed. A few times. I went back to Flexiparking, and I discovered a hidden popup box that only appears if the app is in the background. What a bad UX/UI. And the message? Look below.

I was stuck with a conundrum. I want to pay for parking, but the apps not working. What if I get summoned for not paying parking? Can I sue the app for not being available? (Well they are holding my money in the ewallet which I use specifically for this purpose). Will the app cover for me then? I am the innocent bystander stuck, and the city council no longer has manual tickets to use for parking. Can I take action against city council for failing to provide a manual alternative since the online method is down yet the rules are being enforced?

So many questions!

In the end...

While eyeballing my car, I gobbled up my food and drink and quickly left to avoid any issues.

Update 30 June 2026 1430

It seems that the parking services was indeed down, the following notifications confirms.

5. Where to, next?

The ancient civilization left us with physical documents, while being way advanced than what we are today. Wall carvings, ancient scrolls in parchments. Perhaps they saw something we have yet to realise. Or maybe, they did the same mistake, information might have been stored in some media scattered all over the world isn't readable because we neither understand the language of the technology for it? Maybe an innocent looking rock contains terabyte of information from the uneven surface which seemed completely random?

It's time we re-evaluate digital for what it as. Holistically, and not just because its the in-thing or the sexy KPI some top brass wanrs to achieve.

Author: ORCID ID - Suresh Ramasamy: 0000-0003-4562-037X

This article is mirrored in Linkedin at https://www.linkedin.com/pulse/downfall-digital-ramasamy-cissp-cism-gcti-gnfa-gcda-cipm-wrfse